The Recall Roundup is a monthly survey of regulatory activity affecting the manufacture, distribution, and sale of consumer products. Subject matter may include the latest product recalls, major federal agency developments, and proposed or new federal rules. The blog’s goal is to provide an overview, rather than a comprehensive report on every development that could potentially affect businesses or consumers. Nothing herein constitutes legal advice. If you have questions or comments about the blog, please reach out to the authors.

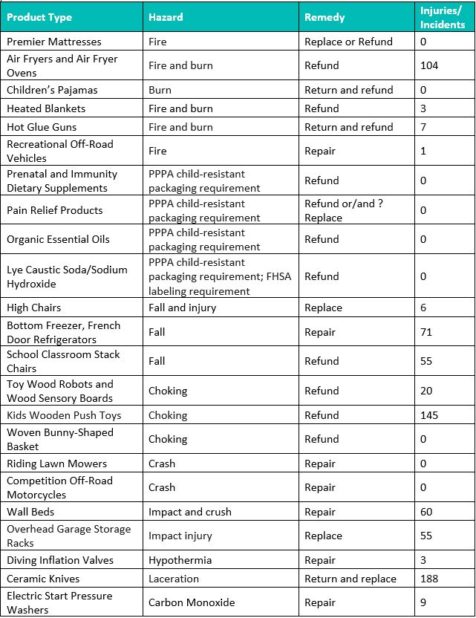

Installation issues seem to be at the heart of an April recall of approximately 129,000 Murphy wall beds announced by Bestar and the US Consumer Product Safety Commission. The recall announcement points to “serious impact and crushing hazards” posed by the beds. At the time the recall was announced, Bestar had received reports of 61 incidents, including the death of a 79-year-old woman after a Bestar wall bed fell on her. Rather than describing a specific defect in the product itself, the recall advises consumers “who are uncertain whether their wall bed needs to be reinstalled” to contact Bestar for a free inspection and, if required, free professional reinstallations. The beds were sold online at a variety of popular online marketplaces, including Wayfair.com, Costco.com, Cymax.com, and Amazon.com.

Three recalls in April serve as a reminder that small parts always pose a risk of causing a recall-inducing product hazard because small parts can separate from a product, which poses a choking hazard to young children. The products included a woven bunny-shaped basket (because the eyes could detach), a wooden push toy (because the toy’s rolling cylinder could separate and expose the small balls inside the cylinder), and a wooden robot toy and a wooden sensory board toy (because small parts could come loose from the toys). Along similar lines, several products were recalled in April because their packaging was not child-resistant, as required by the Poison Prevention Packaging Act. The products included an essential oil containing methyl salicylate, prenatal and immunity capsules containing iron, hemp seed oil pain relief creams and lotions containing lidocaine, and lye caustic soda containing sodium hydroxide.

Finally, fire and burn hazards remain ever-present sources of risk. Best Buy recalled approximately 635,000 air fryers and air fryer ovens due to several dozen reports of the air fryers catching fire, burning, or melting.

Lawyers from Hunton Andrews Kurth LLP’s insurance coverage practice provide an update on recent recall-related insurance coverage disputes below:

We previously reported on Landec Corp.’s action against its insurers (see here and here), which arises out of the insurers’ denial of coverage for over $5 million in losses related to a government-ordered recall of kale salad products. Since our last update, the court granted the issuers' motion to dismiss the California suit on forum non conveniens grounds. The court concluded that the policy’s Forum Selection Clause requiring any suit be in New York controlled and barred Landec from litigating in California. The court rejected Landec’s argument that the Service of Suit provision specifying that the insurers would submit to “a court” in the United States conflicts with the Forum Selection Clause. In reconciling the two provisions, the court stated that the Service of Suit provision requires the insurers to submit to “a court” but that the Forum Selection Clause identifies the forum of that court. The court also distinguished the holding of another California federal court that reached the opposition conclusion. In that case, the court said, the Service of Suit provision was added by an endorsement that stated it modified the policy, which indicated that it was intended to supplant the Forum Selection Clause; whereas, Landec’s Service of Suit provision was not added by endorsement and there was no indication it was meant to modify the Forum Selection Clause. Thus, Landec will be litigating its coverage dispute in the Empire State.

In Houston Casualty Co. v. Andrew Smith Co., No. 1:22-cv-03615, (May 4, 2022 SDNY), an insurer sued its policyholder seeking a declaration of no coverage under a Product Contamination Insurance Policy in relation to the CDC and FDA’s 2018 public warning of lettuce contaminated with E. coli; the Complaint can be found here. The insurer, Houston Casualty Co. (HCC), issued a policy to Andrew Smith Co. that promised to cover “any actual accidental or unintentional contamination, [or] impairment of Products” where consumption of such products would result in identifiable symptoms of bodily injury. Following the FDA’s warning, Andrew Smith incurred over $500,000 in costs related to lettuce it had harvested that was sold to consumers (the Complaint does not explain the nature of the costs incurred) and turned to HCC for coverage. HCC denied coverage, contending that Andrew Smith had not provided proof of actual contamination of a product, as required under the policy. HCC alleges that numerous tests indicated that none of the lettuce supplied by Andrew Smith was contaminated with E. coli, and that Andrew Smith did not cooperate with HCC’s investigation. HCC did not address whether Andrew Smith’s lettuce was “impair[ed]” in some way. The one count Complaint seeks a declaration that no coverage is owed because Andrew Smith Co. failed to cooperate and because the policy is not triggered. We will continue to monitor this dispute for further developments.

We previously reported on Blue Bell Creameries USA, Inc.’s action against its insurers (see here), which arises out of a Listeria outbreak in 2015. Blue Bell Creameries and its insurers have since filed cross motions for summary judgment on whether Blue Bell’s insurers have a duty to defend a shareholder suit arising from Listeria contamination (Blue Bell’s briefing can be found here, here, and here; insurers’ briefing can be found here, here, and here. In 2015, multiple injuries and deaths were caused by Listeria contamination in Blue Bell ice cream products prompting a significant drop in Blue Bell’s stock. A shareholder derivative suit followed, alleging that Blue Bell’s officers and directors failed to establish a system that would have prevented the contamination. The insurers raise many arguments against coverage, including that the directors and officers are not insured because they were accused of having breached their fiduciary duties to Blue Bell and, therefore, couldn’t have been acting in their capacity as directors and officers. Blue Bell counters that the shareholders specifically allege that the directors and officers were acting in the normal course of the ongoing operation of the company. The insurers also argue that there wasn’t an “occurrence” because the directors and officers allegedly engaged in knowing and willful misconduct, which cannot produce an occurrence. But Blue Bell responded that the shareholders did not allege that the presence of Listeria in the ice cream was intentional, only that they did not respond to reports of contamination. The motions are being considered by the court.

In Golden Taste, Inc. v. Westchester Surplus Lines Insurance Co., No. 1:22-cv-00017 (S.D.N.Y. filed Jan. 3, 2022), Golden Taste sued its insurer, Westchester Surplus Lines, seeking coverage under a Recall Plus Insurance for Consumable Products policy. According to the Complaint, Golden Taste produces a variety of kosher food products, including Healthy Tuna Deluxe, a tuna fish salad product. Golden Taste alleges that, in March 2021, one of its retail clients notified it that there was visible organic growth in Golden Taste’s Healthy Tuna Deluxe product, which necessitated the recall and destruction of the product. Subsequent testing confirmed that Aspergillus spp., Candida Lipolytica, and Penicillium Spp were all present in the product. The policy covered, among other things, the voluntary recall of adulterated products where the consumption of those products would result in bodily injury. Nonetheless, Golden Taste alleged that Westchester Surplus denied coverage because the amount of contaminants found were not found to be dangerous to humans.

In Apex Oil Co. v. Starr Indemnity & Liability Co., No. 6:22-cv-00473 (W.D. La. filed Feb. 15, 2022), Apex Oil sued its insurer, Starr Indemnity, for breach of contract and bad faith following Starr Indemnity’s denial of coverage related to damaged oil. According to the Complaint, Apex Oil shipped oil to a client that was contaminated with potassium, which mixed with the oil that was already in the client’s storage tank and amounted to damage of the client’s oil. Starr Indemnity denied coverage pursuant to a Recall of Products, Work or Impaired Property Exclusion. In addition to its damages, Apex seeks its attorneys’ fees, a statutory penalty equal to 50% of the amount found to be owed and/or two times the damages sustained by Apex for Starr’s bad faith in arbitrarily refusing to pay the claim after a fully sworn proof of loss was provided.

Total Recalls: 17

Hazards: Fire/Burn/Shock (6); PPPA (4); Fall (3); Choking (3); Crash (2); Impact/Injury (2); Hypothermia (1); FHSA (1); Laceration (1); Carbon Monoxide (1)

Partner

PartnerKelly practices as a commercial and regulatory litigator on products liability and post M&A disputes and issues and serves as one of the firm’s Deputy General Counsel focusing on law firm ethics, conflicts, and risk management ...

Partner

PartnerGeoff works closely with corporate policyholders and their directors and officers to resolve high-stakes insurance disputes. He leads the firm’s directors and officers (D&O) insurance and executive protection practice.

As a ...

Partner

PartnerKevin is a commercial litigator focusing on insurance coverage disputes and counseling on behalf of policyholders. His educational background and prior experience as an insurance broker and advisor provide him with a deep ...

Search

Recent Posts

Categories

- Advertising & Marketing

- Bankruptcy

- Class Action

- Competition/Antitrust

- Consumer Protection

- Corporate Governance

- Environmental

- General

- Health Care

- Insurance

- IP

- Labor and Employment

- Mergers & Acquisitions

- News & Events

- Patent Infringement

- Patents

- Privacy & Cybersecurity

- Product Liability

- Real Estate

- Regulatory

- Technology & E-Commerce

Tags

- 29 C.F.R. § 785.48

- 396-r

- 3D Printer

- 3D Printing

- A. Todd Brown

- A.S. Research (ASR)

- Aaron P. Simpson

- Accountability

- Administrative Agencies

- Administrative Exemption

- Advertisers

- Advertising

- Advertising Claims

- Advertising Guidelines

- Advertising Idea

- Agency Guidance

- Agency Principles

- AI Interviewing Platforms

- AI Technology Reviews

- AIA

- Air

- Algorithmic Accountability Act

- Align

- Americans with Disabilities Act

- Americans with Disabilities Act (ADA)

- Andrea DeField

- Ann Marie Buerkle

- Annual Reports

- anti-aging

- Anti-Competitive Marketplace

- Anti-Discrimination

- APEX Agreement

- Arbitration

- Arbitration Agreements

- Arizona

- Arkansas

- Arthritis

- Artificial Intelligence (AI)

- Asbestos

- Assembly Bill 51 (AB 51)

- ATDS

- Athlete Eligibility

- Australia

- Auto-renewals

- Automatic Telephone Dialing System (ATDS)

- Automobile

- Automotive Body Parts Association (ABPA)

- Back to Work Emergency Ordinance

- biased endorsements

- Biden Administration

- Biometric Data

- Biometric Information

- Biometric Information Privacy Act (BIPA)

- BIPA

- Bitcoin

- Blockchain

- Board Diversity Disclosure

- Boards of Directors

- Bonuses

- Braille

- Branding

- Breach

- Breach of Contract

- Business Interruption

- Business Interruption Loss

- Businessowner’s Insurance

- Buy Now, Pay Later

- California

- California Air Resources Board

- California Assembly Bill 2011

- California Employment Laws

- California Fair Employment and Housing Act

- California False Claims Act

- California Labor Code

- California Legislation

- California Senate Bill 6

- California’s Unfair Competition Law

- CalRecycle

- CAMS

- Canada

- Cannabis

- CARB

- CBD

- CBP

- CCPA

- Celebrity Endorsers

- Center for Disease Control (CDC)

- CFIUS

- CGL

- Chatbot

- Children’s Advertising

- Children’s Advertising Review Unit

- Children’s Online Privacy Protection Act (COPPA)

- China

- Christopher J. Dufek

- Christopher W. Hasbrouck

- Christy Kiely

- CIPA

- Class Action

- Class Action Litigation

- Class Actions

- Clawback

- Click-to-Cancel

- Climate Change

- Climate Disclosure

- clinical trials

- Collective Action

- Colorado

- Commerce Clause

- Commercial General Liability

- Commercial Leasing

- Commercial Messaging

- Commercial Products

- Commercial Real Estate

- Commodity Futures Trading Commission

- Compensation

- Compliance

- Confidentiality

- Congress

- Connecticut

- Consent

- Consent Order

- Consumer Advertising

- Consumer Data

- Consumer Financial Protection Bureau

- Consumer Fraud

- consumer loyalty program

- Consumer Privacy

- Consumer Product Safety Act

- Consumer Products

- Consumer Products Safety Commission (CPSC)

- Consumer Protection

- Consumer Review Fairness Act of 2016 (CRFA)

- Consumer Reviews

- Consumer Rights

- Contamination

- Contract Law

- Controlled Substance Act

- Cookies

- Cookware

- COPPA

- Copyright

- Coronavirus/COVID-19

- Corp Fin

- Corporate Governance

- Corporate Reporting

- Corporate Sustainability

- Corporate Transparency Act (CTA)

- Costco

- Counterfeit Goods

- Counterfeit Goods Seizure Act of 2019

- Court of International Trade

- CPPA

- CPRA

- CPSA

- CPSC

- Crack House Statute

- CRFA

- Crypto

- Cryptocurrency

- CSPA

- Cuba

- Currency

- Customs and Border Protection

- Cyber

- Cyber Coverage

- D. Andrew Quigley

- D&O

- D&O policies

- Damages

- Data Breach

- Davidson

- Deceptive Advertising

- DEI

- Delaware

- Delivery Drivers

- DEP

- Department of Agriculture

- Department of Justice

- Department of Labor

- Development Impact Fee

- Dietary Guidelines

- Digital Assets

- digital currency

- Disclosures

- Discrimination

- Distribution

- District of Columbia

- Division of Corporation Finance

- Dodd-Frank

- DOJ

- DOL

- Duty to Defend

- Duty to Indemnify

- e-liquid products

- Eddie Bauer

- EEOC

- Electric Vehicles

- Eleventh Circuit

- Emily Burkhardt Vicente

- Employee Rights

- Employment-Based Immigration

- Endorsement

- Endorsement Guides

- Endorsement Notice

- Endorsements

- endorser monitoring requirements

- Enforcement

- Environmental Impact

- Environmental Protection Agency

- Environmental Protection Agency (EPA)

- EPA

- Epidemic

- ESG

- ESG Disclosure

- EU Regulation

- European Union

- European Unitary Patent

- EV Charging

- Exceptions

- Exclusions

- Executive Compensation Disclosure Rules

- Executive Order (EO)

- Executive Orders

- Exercise Machines

- Extended Producer Responsibility (EPR)

- FAA

- Fair Labor Standards Act

- Fair Labor Standards Act (FLSA)

- fair use

- False Advertising

- False Advertising Claims

- False Advertising Law

- False Claims Act

- Family Leave Policies

- FAR

- Fashion Accountability Acts

- FCC

- FCRA

- FDA

- Federal Acquisition Regulations

- Federal Arbitration Act (FAA)

- Federal Communications Commission

- Federal Contractors

- Federal Contracts

- Federal District Court

- Federal Government Contractor

- Federal Government Shutdown

- Federal Trade Commission

- Federal Trade Commission (FTC)

- FFDCA

- FIFRA

- Fifth Circuit

- Final Rule

- Financial Technology

- FinCEN

- FinHub

- Fireworks

- First Amendment

- Fixing America’s Surface Transportation (FAST) Act

- Florida

- Florida House of Representatives (HB 963) and Florida Senate (SB 1670)

- Florida Legislature

- FLSA

- FLSA/Wage & Hour

- FMLA

- Food and Beverage Manufacturers

- Food and Drug Administration (FDA)

- Food Delivery

- Food Safety

- Form 10-K

- Formaldehyde Standards for Composite Wood Products Act of 2010

- fractional interests

- Franchise

- Frederic Chang

- Free Trials

- FTC

- FTC Act

- Gavin Newsom

- GDPR

- General Liability

- Geoffrey B. Fehling

- Georgia

- Gift Cards

- GoodRx

- Gramm-Leach-Bliley (GLB) Act

- Green

- Green Guides

- Greenhouse Gas

- Gun Safety

- Hart-Scott-Rodino

- Hart-Scott-Rodino (HSR)

- Hashtag

- Hawaii

- Health Care

- Health Claims

- Hedge Fund

- Higher Education

- HIPAA

- hoverboards

- human capital

- Human Rights

- IEEPA

- Illinois

- Illinois Artificial Intelligence Video Interview Act (the Illinois Act)

- Illinois Biometric Information Privacy Act (BIPA)

- Independent Contractors

- Indiana

- Indoor Mall

- Influencer Marketing

- Infringement

- initial public offerings (IPOs)

- Injury

- Insurance

- Insurance Loss

- Insurance Provider

- Intellectual Property

- Intellectual Property Licenses in Bankruptcy Act

- Inter Partes Review

- Interest Rate

- International

- International Trade Commission

- International Trade Commission (ITC)

- Internet

- Inventorship

- investigation

- INVISALIGN

- Iowa

- IP

- IPR

- Ireland

- IT

- ITC

- iTERO

- Job Posting

- Joint Employer

- Junk Fees

- Katherine Miller

- Kurt A. Powell

- Kurt G. Larkin

- Labeling

- Labeling Requirements

- Labeling Rules

- Labor

- Labor Code Private Attorneys General Act of 2004 (PAGA)

- Labor Organizing

- Labor Unions

- Land Use

- Landlord

- Latin America

- Lautenberg Act

- Lawsuit Reform Alliance of New York (LRANY)

- Lead

- Lease

- Legislation

- Leveraged Loans

- Liability Insurance Policy

- Liberty Insurance Corporation

- Liberty Mutual Fire Insurance Company

- LIBOR Discontinuation

- liquidity

- Litigation

- Live Chat

- Lost Profits

- Lost Sales

- Louisiana

- Luxury Gyms

- M&A

- Made in the USA

- Made in USA

- MagicSleeve

- Magnuson-Moss Warranty Act

- Magnuson-Moss Warranty Act (MMWA)

- Maine

- Malcolm C. Weiss

- Manufacturing

- Marketing

- Marketing Claims

- Maryland

- Massachusetts

- Matthew T. McLellan

- Maya M. Eckstein

- MD&A

- Medtail

- Membership cancellation

- Mergers & Acquisitions

- Metaverse

- MeToo Movement

- Mexico

- Michael J. Mueller

- Michael S. Levine

- microplastics

- Microplastics Litigation

- Minimum Wage

- Minnesota

- Minnesota Pollution Control Agency (MPCA)

- Misclassification

- Mislabeling

- Mission Product Holdings

- Missouri

- Mobile

- Mobile App

- Motoclick

- Multi-Family Housing Development

- Multi-Level Marketing Program (MLM)

- NAA

- NAD

- NASA

- Nasdaq

- National Advertising Division

- National Advertising Division (NAD)

- National Advertising Review Board

- National Collegiate Athletic Association (NCAA)

- National Labor Relations Act

- National Labor Relations Board

- National Products Inc.

- National Retail Federation

- Natural Disaster

- Nebraska

- Negligence Claims

- Neil K. Gilman

- Network Outage

- Nevada

- New Jersey

- New York

- New York City Department of Consumer and Worker Protection

- New York Department of Financial Services

- NHTSA

- NIL rights

- Ninth Circuit

- NLRA

- NLRB

- no-action request

- Non-Compete

- Non-Exempt

- Non-Exempt Employees

- non-fungible token (NFT)

- North Carolina

- Nutrition Labels

- Obama Administration

- Occupational Safety and Health Administration (OSHA)

- Occurrence

- Office of Labor Standards Enforcement

- Ohio

- Oklahoma

- Online Cash Providers

- Online Retailer

- Online Reviews

- Opinion Letters

- Opioids

- Opt-Out

- Oregon

- Overboarding

- Overtime

- Overtime Exemptions

- Ownership

- Packaging

- PAGA

- Pandemic

- Patent

- Patent Infringement

- Patents

- Paul T. Moura

- Pay Equity

- Pay Ratio

- Pay Transparency

- Pay-To-Play Rankings

- Penalty

- Pennsylvania

- Penny Shortage

- Personal and Advertising Injury

- Personal Data

- Personal Information

- Personal Injury

- Personally Identifiable Information

- Pesticides

- PFAS

- Physical Loss or Damage

- Policy

- Predictive Inventory

- price gouging

- Primary and Umbrella Policies

- Privacy

- Privacy Guidelines

- Privacy Policy

- Privacy Protections

- Procurement

- Product Liability

- Product Packaging

- Product Safety

- Prohibition on Sale

- Property Insurance

- Property Rights

- Proposed Legislation

- Proposed Rule

- Proposition 65

- Proxy Access

- proxy materials

- Proxy Statements

- PTAB

- PTO

- Public Accommodations

- Public Companies

- Purdue Pharma

- Randall S. Parks

- Ransomware

- Real Estate

- Recall

- Recalls

- Recording

- Regulation

- Regulation S-K

- Restaurants

- Restrictions

- Restrictive Covenants

- Retail

- Retail Developers

- Retail Development

- Retail Industry Leaders Association

- Retail Litigation Center

- Retail Year in Review

- Retaliation

- Rounding

- Rulemaking

- Ryan A. Glasgow

- Sales Tax

- Salesforce

- SD8 coins

- SEC

- SEC Disclosure

- Second Circuit

- Section 337

- Section 365

- Secure and Fair Enforcement Banking Act of 2019 (“SAFE Banking Act”)

- Securities

- Securities and Exchange Commission

- Securities and Exchange Commission (SEC)

- Securities Exchange Commission

- security checks

- Self-Checkout

- Senate

- Senate Data Handling Report

- Sergio F. Oehninger

- Service Contract Act (SCA)

- Service Interruption

- Service Provider

- SHARE

- Shareholder

- Shareholder Proposals

- Sign-In Wrap Agreement

- Slogan

- Smart Contracts

- SNAP

- Social Media

- Social Media Influencers

- Software

- South Carolina

- South Dakota

- Special Purpose Acquisition Companies (SPACs)

- Sponsors and Gifting

- Sponsorship

- State Attorneys General

- State Law

- State Legislation

- Store Closures

- Strategic Plan

- Subscription Services

- Substantiation

- Substantiation Notice

- Supplier

- Supply Chain

- Supply contracts

- Supply-Chain Operations

- Supreme Court

- Surveillance Pricing

- Sustainability

- Syed S. Ahmad

- Synovia

- Targeted Advertising

- Tariff

- Tax

- TCCWNA

- TCPA

- Technology

- Technology Innovation

- Telemarketing

- Telephone Consumer Protection Act

- Telephone Consumer Protection Act (TCPA)

- Tempnology LLC

- Tenant

- Tennessee

- Terms and Conditions

- Texas

- The Fair Credit Reporting Act (FCRA)

- Third Party Litigation Funding

- Third-Party

- Thomas R. Waskom

- Title VII

- Tokenization

- Tokens

- Toxic Chemicals

- Toxic Substances Control Act

- Toxic Substances Control Act (TSCA)

- Trade Dress

- Trademark

- Trademark Infringement

- Trademark Trial and Appeal Board (TTAB)

- TransUnion

- Travel

- Trends

- Trump Administration

- TSCA

- TSCA Title VI

- U.S. Department of Justice

- U.S. Department of Labor

- U.S. Food and Drug Administration

- U.S. House of Representatives

- U.S. Patent and Trademark Office

- Ultra-Processed Foods

- Umbrella Liability

- Unfair and Deceptive Use

- Union

- Union Organizing

- United Specialty Insurance Company

- Unmanned Aircraft

- Unruh Civil Rights Act

- UPSTO

- US Chamber of Commerce

- US Customs and Border Protection (CBP)

- US Department of Agriculture

- US Environmental Protection Agency (EPA)

- US International Trade Commission (ITC)

- US Origin Claims

- US Patent and Trademark Office

- US Patent and Trademark Office (USPTO)

- US Supreme Court

- USDA

- USPTO

- Utah

- Varidesk

- Vendor

- Vermont

- Virginia

- Volatile Organic Compound (VOC) Emissions

- W. Jeffery Edwards

- Wage and Hour

- Wage-And-Hour

- Walter J. Andrews

- Warning Labels

- Warranties

- Warranty

- Washington

- Washington DC

- WCAG

- Web Accessibility

- Website

- Website Accessibility

- Weight Loss

- Wiretap

- Wiretapping

- World Health Organization (WHO)

- Wyoming

- Year In Review

- Zoning

- Zoning Conversion

- Zoning Ordinances

- Zoning Regulations

Authors

- Gary A. Abelev

- Christian S. Adams

- Syed S. Ahmad

- Brandon Bell

- Fawaz A. Bham

- Michael J. “Jack” Bisceglia

- Jennifer L. Bloom

- Jeremy S. Boczko

- Brian J. Bosworth

- Shannon S. Broome

- Samuel L. Brown

- Tyler P. Brown

- Melinda Brunger

- Jimmy Bui

- M. Brett Burns

- Daniel J. Butler

- Matthew J. Calvert

- Grant H. Cokeley

- Eric S. Crusius

- Christopher J. Cunio

- Alexandra B. Cunningham

- Merideth Snow Daly

- Timothy G. Decker

- Katherine P. Deegan

- Andrea DeField

- John J. Delionado

- Stephen P. Demm

- Mayme Donohue

- Christopher J. Dufek

- Robert T. Dumbacher

- M. Kaylan Dunn

- Chloe Dupre

- Frederick R. Eames

- Andre Earls

- Maya M. Eckstein

- Rob Edwards

- Tara L. Elgie

- Clare Ellis

- Latosha M. Ellis

- Juan C. Enjamio

- Kelly L. Faglioni

- Ozzie A. Farres

- Geoffrey B. Fehling

- Jason Feingertz

- Hannah Flint

- Erin F. Fonté

- Kevin E. Gaunt

- Jane M. Geiger

- Andrew G. Geyer

- Armin Ghiam

- Neil K. Gilman

- Ryan A. Glasgow

- Tonya M. Gray

- Elisabeth R. Gunther

- Steven M. Haas

- Kevin Hahm

- Jason W. Harbour

- Jeffrey L. Harvey

- Christopher W. Hasbrouck

- Eileen Henderson

- Gregory G. Hesse

- Kirk A. Hornbeck

- Jamie Zysk Isani

- Nicole R. Johnson

- Roland M. Juarez

- James A. Kennedy, II

- Suzan Kern

- Jason J. Kim

- Scott H. Kimpel

- Elizabeth King

- Abigail Klauer

- Leslie W. Kostyshak

- P. Reiko Koyama

- Kurt G. Larkin

- Tyler S. Laughinghouse

- Gerry Leone

- Michael S. Levine

- Ashley Lewis

- Abigail M. Lyle

- Maeve Malik

- Sadie Mapstone

- Eric R. Markus

- John Gary Maynard, III

- Gray Moeller

- Reilly C. Moore

- Michael D. Morfey

- Ann Marie Mortimer

- Michael J. Mueller

- J. Drei Munar

- Matthew Nigriny

- Michael A. Oakes

- Justin F. Paget

- Randall S. Parks

- J. Steven Patterson

- Katherine C. Pickens

- Gregory L. Porter

- Robert T. Quackenboss

- D. Andrew Quigley

- Michael Reed

- Natalie Reed

- Jonathan D. Reichman

- Kelli Regan Rice

- Patrick L. Robson

- Amber M. Rogers

- Zachary Roop

- Adam J. Rosser

- Rachel Saltzman

- Natalia San Juan

- Arthur E. Schmalz

- Raymond Schorr

- Daniel G. Shanley

- Madison W. Sherrill

- Nikki Skolnekovich

- Kevin V. Small

- J.R. Smith

- Bennett Sooy

- Brian T. Stansbury

- Daniel Stefany

- Hak Stepanyan

- Javaneh S. Tarter

- Shauna R. Twohig

- Paige Van Oosten

- Jessica N. Vara

- Emily Burkhardt Vicente

- Mark R. Vowell

- Gregory R. Wall

- Thomas R. Waskom

- Malcolm C. Weiss

- Holly H. Williamson

- Samuel Wolff

- Jingyi “Alice” Yao

- Jessica G. Yeshman