We have written extensively on the US Securities and Exchange Commission (SEC) proposal to require that public companies disclose climate-related information and other environment, social, and corporate governance (ESG) trends. However, the European Union (EU) is at the vanguard of emerging requirements focused on climate-related information and broader ESG-aligned information.

Recent and forthcoming regulatory developments will have significant implications not just for EU-based companies but for those beyond, as well. Late last month, the European Parliament and Council of the EU announced they have reached political agreement to move forward with and expand applicability of a proposed measure that would require corporate sustainability reporting from a vastly increased number of companies. This change and others could have important impacts on businesses that merit close attention, including by non-EU companies. This post is meant to provide a quick primer on the EU’s array of trending ESG efforts and preview what additional requirements are expected in the future.

Backdrop of EU Sustainable Finance Framework

The EU ESG efforts dovetail with its mission to deliver on the European Green Deal, the aggressive, whole-economy approach to make Europe the first carbon neutral continent on the globe by 2050, and its intermediate goal of reducing greenhouse gas (GHG) emissions by at least 55 percent compared with 1990 levels by 2030, codified in the European Climate Law. The EU believes sustainable finance is a key component of its ability to achieve these targets. The “sustainable finance” framework encompasses a range of initiatives aimed at harnessing investment toward a clean economy, including:

- The Taxonomy Regulation establishes a classification system indicating which economic activities, across a wide range of industries, are environmentally sustainable. Whether an activity is identified as sustainable depends on whether it makes a “substantial contribution” and does “no significant harm” to a series of environmental objectives, as well as meet certain minimum social safeguards and technical screening criteria.

- The Sustainable Finance Disclosure Regulation (SFDR) imposes ESG disclosure requirements on financial market participants and products in the EU, aimed at protecting investors from greenwashing concerns.

- The Corporate Sustainability Reporting Directive (CSRD), a successor to and expansion of earlier corporate disclosure requirements, will require many large companies and companies with securities listed on EU-regulated markets to disclose a broad array of information under the E, S, and G pillars.

- The Green Bond Standard encourages the issuance of and investment in green bonds to help finance Europe’s low carbon transition by setting a voluntary standard for green bonds to ensure sustainability and investor protections.

- Benchmark labeling and ESG disclosure requirements serve to increase the ESG transparency of benchmark methodologies.

While all of these initiatives could be impactful to companies with European operations, here, we will focus in on the CSRD because of its far-reaching effects that will impact not just EU-based companies but certain US-based companies with operations in the EU and require significant planning to ensure adequate tracking, accounting, and reporting of requisite ESG information.

To whom will the CSRD apply?

Although corporate sustainability disclosure requirements are not new in the EU, the CSRD is a marked expansion. The Non-Financial Reporting Directive (NFRD), which has required certain companies to report for several years, currently applies to fewer than 12,000 large, “public interest” companies (i.e., listed companies, banks, and insurance companies). Under the CSRD, however, it is estimated that nearly 50,000 companies will have to report. That includes:

- all large companies (i.e., those meeting at least two of three criteria: more than 250 employees, greater than €40 million in turnover, and balance sheets above €20 million), whether they are listed on EU regulated markets or not;

- all listed companies (i.e., those offering securities on EU regulated markets), including small and medium-sized enterprises (SMEs) but excluding micro-undertakings (all of which are defined under the EU’s Accounting Directive 2013/34/EU); and

- non-European companies that generate a net turnover of €150 million or more in the EU and have at least one subsidiary or branch in the EU.

The first of these applicability criteria has the potential to draw in the EU subsidiaries of non-EU companies but the third criterion – which was added as part of the political agreement announced last month – makes certain the CSRD’s applicability to some non-EU based companies.

What does the CSRD require?

Subject companies will need to comply with European Sustainability Reporting Standards (ESRS), mandatory EU-wide ESG reporting standards, as well as with certain principles and audit and reporting format requirements.

- European Sustainability Reporting Standards (ESRS)

The standards are still under development by the European Financial Reporting Advisory Group (EFRAG). The initial set of proposed reporting standards are due to be released later this year, and adopted next summer, specifying disclosure requirements under ESG pillars on a “sector agnostic” basis. A further set of “sector specific” standards is due to follow after that.

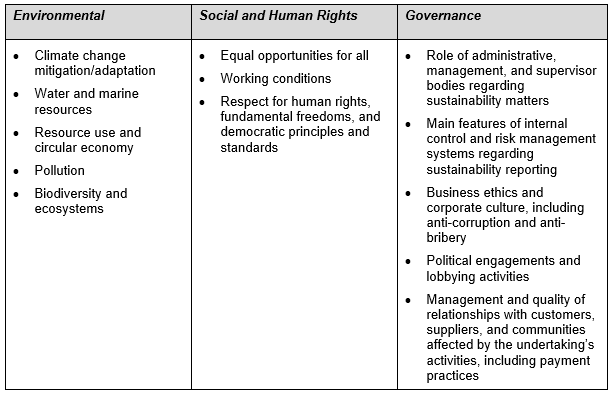

The EFRAG has issued a “roadmap” for development of the standards and a series of working papers, however, indicating the contents of at least some of the ESRS. Generally, the ESRS will require a myriad of disclosures falling within certain categories under each of the “E,” “S,” and “G” pillars, listed below:

Within each of these reporting standard areas, companies would need to make disclosures related to strategy (i.e., strategy and business model, governance and organization, impacts, risks, and opportunities), implementation (i.e., policies, targets, action plans, and resources), and performance measurement.

- Double Materiality

Because of these twin aims of informing both investors and the public, the CSRD is based on the principle of “double materiality” – meaning that companies need to disclose not just effects of ESG factors on its own operations (i.e., inward looking) but also their operations’ effects on sustainability goals (i.e., outward looking).

- Third Party Assurance

The CSRD proposal would also impose a third party assurance or audit requirement for sustainability information. At first, companies would need only provide “limited assurance.” Later, however, the proposal contemplates that a more rigorous “reasonable assurance” would be required.

- Reporting Format

Rather than releasing a separate “sustainability report,” the CSRD will require that all necessary disclosures are presented in a separate section within a company’s management report. The goal of this is to reinforce the importance of sustainability information and provide for consolidated financial and sustainability information. Also, for groups of related companies subject to the CSRD, a single, consolidated report can satisfy the reporting requirements. Additionally, the sustainability information will need to be digitally “tagged” to allow for the information to be fed into a single access point database.

Why the expansion of the CSRD?

A couple of motives are driving the CSRD. One is to ensure sustainability information is available to entities subject to SFDR requirements. The SFDR was adopted in 2019, and initial disclosure requirements are already in force, but requirements under the SFDR are evolving. This past spring, for example, the European Commission adopted a Delegated Regulation to supplement the SFDR and prescribe the specific content, methodology, and presentation of information to be disclosed. If agreed to by the European Parliament and the Council, the updated SFDR requirements would apply beginning starting next year. But financial market participants subject to the expanding SFDR requirements are finding themselves in a lurch in terms of available data to support their own reporting obligations. The CSRD’s reporting requirements will thus help to provide adequate corporate sustainability information for SFDR compliance.

Another factor is a desire to provide general stakeholders with sustainability information about companies with significant EU operations, which may drive consumer decisions or further policymaking.

Finally, part of the rationale for the addition of non-EU based companies with significant EU operations among the list of subject entities is to help level the playing field between the rigorous regulatory and reporting standards applicable to EU companies and the potentially more relaxed standards for companies based elsewhere.

When will CSRD obligations begin?

The CSRD is slated for final adoption late this year. EU member states would then need to translate the CSRD into their national laws within 18 months. Under the proposal, standards would become applicable first for companies already subject to the NFRD beginning in 2024, with initial reporting due in 2025 for the prior year. Applicability to the remaining subject entities would be staggered:

- Large undertakings would need to comply the following year in 2025 with the first report in 2026;

- SMEs would follow a year later, with applicability beginning in 2026, and reporting starting in 2027; and, finally,

- Non-EU companies covered by the CSRD would be subject starting in 2028, with the initial reporting due in 2029.

How should US companies prepare?

First, US companies should be aware that expanded ESG reporting is coming, and not just from the SEC or emerging state laws. Grasping now that your company may be subject to multiple ESG reporting frameworks is important to institute appropriate strategies to track and account for the information that will need to be gathered to satisfy divergent – or even conflicting – reporting standards.

Next, the CSRD requirements seem onerous – and they are – but, based on the proposal, there is a long lead time before initial reports will be due for non-EU companies subject to the CSRD. Moreover, large, EU-based companies will be required to report long before non-EU companies, and thus to road test the requirements. That should allow non-EU companies subject to the CSRD sufficient time to implement mechanisms to track the necessary information, but also to reap the benefit of others’ work in establishing best practices and experience.

Lastly, keep in mind that things are moving fast in the EU; not just in the ESG space but across the regulatory spectrum through implementation of the European Green Deal. If you have operations or otherwise do significant business in the EU, it is important to stay abreast of developments there that may affect you.

Partner

PartnerAs a former US Environmental Protection Agency (EPA) attorney, Sam utilizes his agency, regulatory, enforcement, and practical experience to help his clients navigate environmental, energy, natural resource, sustainability ...

Partner

PartnerAlexandra focuses on environmental issues across media involving regulation, compliance, enforcement and litigation.

Alexandra represents clients on matters arising under a wide range of federal environmental laws. She ...

Search

Recent Posts

- Advisory Council on Historic Preservation Poised to Propose Course Correction to Streamline Cultural Resources and Tribal Consultation

- Federal Court Enjoins Enforcement of California’s Truth in Recycling Law: What This Means for Businesses

- CARB Holds Public Workshop on Regulatory Concepts for Reporting Under California SB 253

Categories

- Agreements

- Air

- Batteries

- California

- Carbon

- Carbon Markets

- CERCLA

- Chemicals

- Climate

- Coal

- Duty to Defend

- Election

- Endangered Species

- Energy Transition

- Enforcement

- Environmental

- Environmental Justice

- Environmental Law

- EPA

- ESG

- General

- General Liability

- Manufacturing

- Mining

- Natural Resources

- Oil & Gas

- Permitting

- PFAS

- Policy

- Renewables

- Trade Agreements

- Utilities

- Waste

- Water

Tags

- 2015 Standards

- 2018 Farm Bill

- 2020 Presidential Election

- 2022 Scoping Plan for Achieving Carbon Neutrality

- 316(b)

- 3D Printer

- 3D Printing

- 4(d) Rule

- 404

- 404 permits

- 404(g)

- 45Q

- AB 1200

- AB 2503

- AB 617

- Abeyance

- ABS

- ACE

- Acrylonitrile-Butadiene-Sytrene

- Active Guidance

- ADAO

- Adaptation

- Adjacent

- Administration

- Administrative Agencies

- Administrative Law

- Administrative Procedure Act

- Administrator Pruitt

- Adverse Modification

- Advertising

- Advisory Opinions

- Affordable Clean Energy

- Aftermarket Parts

- Agency

- Agency Budget

- Agency Finance

- Agency for Toxic Substances and Disease Registry

- Agency Guidance

- Agency Interpretation

- Agent

- Agriculture Improvement Act of 2018

- Air

- Air Emissions

- Air Permit

- Air Pollution

- Air Quality

- Air Quality Implementation Plan

- Air Quality Management District

- Air Quality Management Plan

- ALARP

- Alexandria Ocasio-Cortez

- Algae

- Allco Finance Unlimited v. Klee

- Allegheny

- Alternative Energy Portfolio

- Alternative Energy Portfolio Standard

- Ambient Air

- Amendments

- America's Water Infrastructure Act

- American Bar Association

- American Jobs Plan

- AMLO

- Anadarko Petroleum

- Andrés Manuel López Obrador

- Annie Kuster

- Anthony Kennedy

- Anti-Backsliding

- Anti-terrorism

- Antibacterial

- Antitrust

- AOC

- APA

- Appropriations

- APS

- AQMP

- Aquaculture

- Arbitration

- Arctice Grayling

- Arizona

- Army Corps of Engineers

- ARPA-E

- Articles

- Artificial Intelligence (AI)

- Artificial Island transmission project

- Asbestos

- Asbestos Disease Awareness Organization

- Assumption

- Atlantic Coast Natural Gas Pipeline

- Audubon Society

- Auer

- Auer Deference

- Automobile

- Autonomous Vehicles

- Auxiliary Emissions Control Devices

- Aviation

- BAAQMD

- Backstop Siting

- Backup generators

- BACT

- Bag Ban

- Bald and Golden Eagle Protection Act

- Bankruptcy

- BART

- Baseload

- Batteries

- battery storage

- Bay Area Air Quality Management District

- Beauty products

- Beneficial Use

- Beneficial Use and Reuse

- Bernie Sanders

- Best Available Control Technologies

- Beto O'Rourke

- BGEPA

- Biden Administration

- Bilateral Investment Treaty

- Biological Opinion

- Bipartisan Budget Act

- BIT

- Black-Capped Vireo

- BLM

- Blue Ribbon Task Force

- BOEM

- BOP

- Boston

- Boundary

- Brand Memo

- Brent Spar

- Brett Kavanaugh

- Brownfields

- BSEE

- Budget Proposal

- Bureau of Land Management

- Bureau of Ocean Energy Management

- CAA

- CAISO

- Cal-OSHA

- CalEPA

- California

- California Air Resources Board

- California Coastal Act

- California Consumer Protection Act of 2018

- California Department of Public Health

- California Department of Toxic Substances

- California Environmental Protection Agency (CalEPA)

- California Environmental Public Health and Workers Defense Act of 2019

- California Environmental Quality Act

- California Law

- California Legislature

- California Mining

- California Ocean Protection Council

- California OEHHA

- California Proposition 13

- California Proposition 65

- California Regional Water Quality Control Boards

- California State Lands Commission

- California State Water Resources Control Board

- California Superior Courts

- California Title 8

- California Water Code section 13304

- California-China Clean Technology Partnership

- California's Safe Drinking Water and Toxic Enforcement Act

- CalRecycle

- Canada

- Cannabis

- Cap In Place

- Cap-and-Trade

- Capital Asset Pricing Model

- CAPP

- CARB

- Carbon Capture

- Carbon Capture and Sequestration

- Carbon Capture Demonstration Projects Program

- Carbon Capture Large-Scale Pilot Projects

- Carbon Capture Utilization and Storage

- Carbon Credits

- Carbon Dioxide

- Carbon Dioxide Removal

- Carbon Intensity

- Carbon Markets

- Carbon Nanotubes

- Carbon Utilization

- CASAC

- Categorical Exclusion

- CBD

- CBI

- CCPA

- CCPS

- CCR

- CCR Rule

- CCS

- CCS Alliance

- CCUS

- CDP

- CDR

- CECP

- CEJST

- Center for Chemical Process Safety

- Centralized Waste Treatment

- CEQ

- CEQA

- CERCLA

- Certificate of Public Convenience and Necessity

- Certification

- Certified Unified Program Agencies

- CESER

- CFATS

- CFCs

- CFE

- CGL

- Chambers USA

- Chapter 91

- Chemical

- Chemical Data Reporting

- Chemical Exposure

- Chemical Risk Assessment

- Chemical Safety Board

- Chemicals

- Cheryl LaFleur

- Chevron Deference

- Cheyenne River Sioux

- Chloroflourocarbons

- Chlorpyrifos

- Chrysotile Asbestos

- CIP

- Circular Economy

- CITES

- Citizen Petition

- Citizen Suit

- Civil Penalties

- Civiletti

- Claims-Made

- Class VI

- Class VI Primacy

- Class VI Underground Injection Control

- Clean Air Act

- Clean Development Mechanism

- Clean Energy

- Clean Energy Resources

- Clean Energy Standard

- Clean Hydrogen

- Clean Peak Energy Certificates

- Clean Power Plan

- Clean Water Act

- Clean Water Act Section 401

- Clean Water Act Section 404

- Cleaning Products

- Cleanup

- Climate

- Climate Change

- Climate Disclosure

- Closure by Removal

- CNTs

- CO2

- CO2 Emissions

- Coakley Order

- Coal

- Coal Ash

- Coal Ash Basins

- Coal Combustion Residuals

- Coal Leasing Moratorium

- Coal Mine Health and Safety Act

- Coal Production

- Coalition for Competitive Electricity v. Zibelman

- Coastal

- Coastal Zone Management Act

- Colorado

- Comisión Federal de Electricidad

- Commercial General Liability

- Commercial Information

- Common Law

- Community Air Protection Program

- Compliance

- Comprehensive Environmental Response Compensation and Liability Act

- concurrent-remedies doctrine

- Confidential Business Information

- Congress

- Congressional Research Service

- Congressional Review Act

- Consent Decree

- Conservation Easement

- Considerations

- Constitutional Law

- Consultation

- Consumer Data

- Consumer Product Exposure Warnings

- Consumer Products

- Consumer Products Safety Commission

- Contaminated Sites

- Contribution Threshold

- Controlled Substances Act of 1970

- Cook Inlet

- Cookware

- Cooling Water Intake Structures

- Cooperative Federalism

- COP26

- COP28

- COP28 Agreement

- Coronavirus/COVID-19

- Corporate Governance

- Corporate Social Responsibility

- Corporate Sustainability

- Corporate Sustainability Reporting Directive

- Corporate Sustainability Reporting Directive (CSRD)

- Corporate Valuation

- Corps

- Cosmetics

- Cost of regulation

- Council on Environmental Quality

- County of Maui

- COVID-19

- CPCN

- CPECs

- CPP

- CPS

- CPSC

- CPUC

- CRA

- Criminal Enforcement

- Critical Electric Infrastructure Information

- Critical Habitat

- Critical Habitat Designation

- Critical Infrastructure

- Critical Infrastructure Protection

- Critical Materials

- Critical Minerals

- Critical Minerals Committee

- Cross-State Air Pollution Rule

- CSA

- CSAG

- CSAPR

- CSB

- CSR

- CSR reports

- CSR Standards

- CSR- and ESG-related risks

- Cultural Resources

- CWA

- CWA Citizen Suit

- CWA section 401

- CWA Section 404

- Cyber-Related Risks

- Cybersecurity

- D&O

- D&O Insurance

- Dakota Access Pipeline

- DAPL

- DARTIC

- Data

- Data Centers

- Data Security

- DC Circuit

- DC Circuit Court of Appeals

- DCH

- Deadline Suits

- Deadlines

- Decarbonization

- Decommissioning

- Deep-Well Injection

- Defeat Devices

- Defense Costs

- Deference

- Deidre G. Duncan

- Delisting

- Democratic Debate

- DEP

- Department of Defense

- Department of Energy

- Department of Homeland Security (DHS)

- Department of Justice

- Department of Justice (DOJ)

- Department of Labor

- Department of the Interior

- Department of Transportation

- Designations

- Development

- Device

- Diligent Prosecution

- Dioxane

- Director’s Order

- Directors & Officers

- Discharge

- Diversity and Inclusion

- DJSI

- DOD

- DOE

- DOER

- DOI

- DOJ

- DOJ ENRD

- Domestic Energy Policy

- Domestic Terrorism

- DOSH

- DOT

- Dow Jones Sustainability Index

- DPR

- DPU

- Draft

- Draft EA

- Draft Environmental Assessment

- drinking water

- Drinking Water Standards

- Drought

- DTSC

- Due Diligence

- Duke Energy

- Duty to Defend

- Dynamic Scoring

- E&P Wastes

- EA

- eagle

- Eagle Take Permit

- Earth Day

- Economic Impact

- Economic Impacts

- Effluent

- Effluent Guidelines

- Effluent Limitations

- EHSS

- EIS

- EJSCREEN

- Election 2020

- Electric Ratepayers

- Electric Transmission

- Electric Vehicles

- Electricity

- Electricity Markets

- ELG

- ELGs

- Elizabeth E. Aldridge

- Elizabeth Warren

- Emergency generators

- Emergency Planning and Community Right-to-Know Act

- Emergency Response

- Emergency Support Functions

- Emerging Contaminants

- Emission Caps

- Emission Control Requirements

- Emission Reduction Credits

- Emissions

- Emissions Caps

- emissions reporting

- Emphasis List

- Endangered Species

- Endangered Species Act

- Energy

- Energy Dominance Financing

- Energy Industry

- Energy Infrastructure

- Energy Loan Programs Office

- Energy Package Insurance

- Energy Policy Act

- Energy Reforms

- Energy Storage

- Energy Transition

- Enforcement

- Enforcement Discretion

- Enforcement statistics

- Engine Certification

- Enhanced Oil Recovery

- ENRD

- Environment

- Environment and Natural Resources Division

- Environmental

- Environmental and Social Governance

- Environmental Appeals Board

- Environmental Assessment

- Environmental Bar

- Environmental Compliance

- Environmental Crimes

- Environmental Defense Fund

- Environmental Disclosure

- Environmental Due Diligence

- Environmental Enforcement

- Environmental Groups

- Environmental Impact Statement

- Environmental Justice

- Environmental Justice and Equity Board

- Environmental Law

- Environmental Law Institute

- Environmental Markets

- Environmental Permitting

- Environmental Protection Agency

- Environmental Protection Agency (EPA)

- Environmental Rights

- Environmental Social and Corporate Governance

- Environmental Social and Governance

- Environmental Social Governance

- Environmental Social Justice

- Environmental Transactions

- EO 13891

- EOR

- EP3

- EP4

- EPA

- EPA audit policy

- EPR

- EPR Laws

- Equator Principles

- Equator Principles Association

- ERC

- ESA

- ESA consultation

- ESA section 7 consultation

- ESG

- ESG Diligence

- ETP

- EU

- European Climate Law

- European Green Deal

- European Sustainability Reporting Standards

- European Union

- Evaluation of Regionalization for Potential New Wastewater Systems

- EVs

- Exceptional Events

- Exceptional Events Rule

- Excess Insurance

- Excess Liability

- Exchange Act

- Executive Compensation

- Executive Memorandum

- Executive Office for United States Attorneys

- Executive Order (EO)

- Executive Order 13777

- Executive Order 14008

- Executive Order N-8-23

- Executive Orders

- Exemption

- Extended producer Responsibility

- Extended Producer Responsibility (EPR)

- Fair and Equitable Treatment

- Fair Labor Standards Act

- FAR

- Farmers

- Fashion Accountability Acts

- FAST Act

- FAST-41

- Fathead Minnow

- Fatmucket Mussel

- FDA

- FECM

- Federal Acquisition Regulations

- Federal Action

- Federal Agencies

- Federal Agency Action

- Federal Agency Rulemaking

- Federal Aviation Administration

- Federal Budget

- Federal Energy Regulatory Commission

- Federal Lands

- Federal Permit

- Federal Power Act

- Federal Preemption

- Federal Register

- Federal Rule 20

- Federal Rule 71.1

- Federalism

- Fees

- FERC

- FET

- Fiduciary Liability

- FIFRA

- Fifth Circuit

- Final Rule

- Financial Information

- Fireworks

- First Amendment

- Fishing Industry

- Flaring

- Flint

- FloaTEC LLC

- Flood Infrastructure Funding

- Flood Mitigation

- Florida

- FLSA

- FOIA

- Food

- Food and Beverage Manufacturers

- Food and Drug Administration

- Food and Drug Administration (FDA)

- Food Loss and Waste

- Food Marketing Institute

- Food Marketing Institute v. Argus Leader Media

- Food Waste

- Food Waste Reduction Alliance

- Fossil Fuels

- Fourth Circuit

- Fourth of July

- FPA

- FPA Preemption

- FPA section 202(c)

- FPOS

- Fracking

- Framework

- Framework Rule

- Fraud

- Free Trade Agreement

- Freedom of Information Act

- Freeport

- FSLA

- FTA

- Funding for Environmental Protection

- Funding Mechanism

- FUTURE Act

- FWS

- FY2017 budget

- FY2018

- GAO

- Gas

- GDPR

- Gender Equality

- General Data Protection Regulation

- General Industrial Stormwater Permit

- General Permit

- GenX

- George Clemon Freeman Jr.

- GHG

- GHG Emissions

- GHG Emissions Renewable Portfolio Standard

- Gilbert & Sullivan

- Global Carbon Markets

- Global Climate Negotiations

- Global Reporting Initiative

- Global Warming Solutions Act

- Glyphosate

- GOM

- Good Neighbor Obligation

- Good Neighbor Provision

- Government Investigations

- Grand River Dam Authority

- Grassroots Activisim

- Green Admendment

- Green Communities Act

- Green Deal

- Green New Deal

- Green New Deal; Climate Change

- Greenhouse Gas

- Greenhouse Gas Emissions

- Greenhouse Gas Protocol

- Greenhouse Gas Protocol Initiative

- Greenhouse Gases

- Grid

- Grid Connection and Congestion Management Act

- grid reliability

- grid study

- Grocery Manufacturers Association

- Groundwater

- Guam

- Guidance

- Guidance Portal

- Gulf of Mexico

- Habitat

- Hardrock Mining Rule

- Harmful Algal Blooms

- Hawaii

- Hawkes

- Hazardous Air Pollutants

- Hazardous Materials Regulations

- Hazardous Waste

- HBCD

- HCFCs

- Health

- Health Advisories

- Health Advisory

- Health and Safety

- HECT

- Hemp

- HFCs

- High-Density Polyethylene (HDPE)

- Highly Reactive Volatile Organic Compound Emissions Cap and Trade

- Historical Matter

- HMR

- Holder

- Homeland Security

- Hoopa Valley Tribe

- House

- House of Representatives

- Houston Casualty

- Human Health Toxicity Values

- Human Rights

- Hurricane Harvey

- Hydraulic Fracturing

- Hydroelectric Relicensing

- Hydrofluorocarbons

- Hydrofluorocarbons (HFCs)

- Hydrogen

- Hydrogen Energy Earthshot

- Hydrological Connection Theory

- Hydropower

- ICMM

- ICSID

- IFC Performance Standards

- IGP

- IIA

- IIJA

- Impaired Waterbodies

- Impaired Waters

- Impairment

- Incident Response

- Incidental Take

- incidental take statement

- Indian Lands

- Indigenous Traditional Ecological Knowledge

- Indonesia

- Industrial Accidents

- Industrial Hemp

- Infectious Disease Preparedness and Response Plan

- Inflaction Reduction Act

- Infrastructure

- Infrastructure Development

- Infrastructure Investment and Jobs Act (IIJA)

- infrastructure security

- Initial & Boundary

- Innovation

- Inside Look

- Inspections

- Insurance

- Insurance Recovery

- Integrated Science Assessment

- Interagency Review

- Intergovernmental Panel on Climate Change

- Interior

- International Arbitration

- International Centre for Settlement of Investment Disputes

- International Council on Mining and Metals

- International Energy Agency

- International Environmental Law

- International Investment Agreements

- International Petroleum Industry Environmental Conservation Association

- Interstate Transport

- Intervention

- Investment Risk Assessment

- IPCC

- IRIS

- IRIS Review

- IRS

- ISO-NE

- ISOs

- ITEK

- Jay Inslee

- Jewell

- Joe Biden

- John Hickenlooper

- Joint Venture Provision

- Judicial Review

- Judiciary

- Jurisdiction

- Jurisdictional Determination

- Justice40

- Kamala Harris

- Kavanaugh

- Kenk’s amphipod

- Kevin McIntyre

- Keystone XL

- Kigali Amendment

- Kisor

- Kisor Deference

- Kyoto Protocol

- Lake Erie

- Lake Powell Pipeline Project

- Lampsilis Siliquoidea

- Land Use

- Late Notice

- Lautenberg Act

- Law360

- LCPFAC SNUR

- LDC

- LDNR

- Lead

- Lead and Copper Rule

- Lease Sale

- Legislation

- Lesser Prairie Chicken

- Li-ion

- Liability

- Liability Insured

- Linear

- Liquefied Natural Gas

- Lithium-ion batteries

- Litigation

- Lloyd’s of London

- Lloyds

- LNG

- London Protocol

- Long-Form Warning

- Look-back period

- Louisiana Department of Natural Resources

- Low Carbon Fuel Standard

- MA DOER

- Maine

- Maine Department of Environmental Protection

- Maintenance Fees

- Malaysia

- Manufactured Products

- Manufacturer

- Manufacturers

- Manufacturing

- Marijuana

- Maritime

- Markets

- Masias

- Mass Emissions Cap and Trade

- Massachusetts

- Massachusetts AG

- Massachusetts Clean Energy Center

- Massachusetts Climate Act

- Massachusetts Department of Energy Resources

- Massachusetts Global Warming Solutions Act

- MassCEC

- MATS

- Maximum Contaminant Levels

- MBTA

- MBTA; Wind Energy; Renewable Energy; protected species; natural resources; USFWS

- McGraw-Edison

- McIntyre

- MCL

- MCLG

- MCLs

- McNamee

- MEA

- MECT

- Mergers & Acquisitions

- Methane

- methane emissions

- Methane Repeal Rule

- Methylene Chloride

- Michigan

- microplastics

- Midnight Rule

- Midstream

- Migratory Bird Treaty Act

- Migratory Birds Treaty Act

- Millennium Pipeline

- Mineral Law of 1872

- Mineral Leasing Act

- Mineral Policy

- Mining

- Mining Claims

- Minnesota

- Minnesota Pollution Control Agency (MPCA)

- Misbranding

- Mitigation

- Mitigation Rule

- MLP

- Modification

- Monitoring

- Monsanto

- Montana

- Montreal Protocol

- Moratorium

- MOU

- Mountain Valley Pipeline

- MSGP

- Multi-Sector General Permit

- Multiyear Plan for Energy Sector Cybersecurity

- Mulvaney

- Murray

- Murray Energy

- MVP

- NAAQS

- NAFTA

- NAIOP

- NALs

- Nancy Pelosi

- NATA

- National Ambient Air Quality Standards

- National Compliance Initiatives

- National Cybersecurity and Communications Integration Center

- National Defense Authorization Act

- National Determined Contributions

- National Emergency

- National Enforcement and Compliance Initiatives

- National Enforcement Initiatives

- National Environmental Policy Act

- National Historic Preservation Act

- National Hydro Association

- National Marine Fisheries Service

- National Oceanic Atmospheric Administration

- National Parks and Conservation Ass’n v. Morton

- National Petroleum Council

- National Pollutant Discharge Elimination System

- National Pollutant Discharge Elimination System (NPDES)

- National Pollution Discharge Elimination System

- National Primary Drinking Water Regulation

- National Priorities List

- National Recycling Strategy

- National Register of Historic Places

- National Restaurant Association

- National Security

- Nationwide Permit

- Native American Law

- Natural Gas

- Natural Gas Act

- Natural Gas Leak Abatement Program

- Natural Gas Pipeline Certification

- Natural Gas Pipelines

- Natural Resource Damages

- Natural Resources

- Navigable waters

- NCCIC

- NCI

- NEC

- NECIs

- NEI

- Neil Chatterjee

- NELs

- NEPA

- NEPA Policy

- NEPA Review

- NERC

- NESCOE

- Net-Zero Emissions

- Net-Zero Greenhouse Gas Emissions

- New Chemicals Review Program

- New Rule

- New Source Review

- New York

- New York Department of Environmental Conservation

- New York State Department of Taxation and Finance

- NGA

- NGO

- NHPA

- NHTSA

- NIETC

- Ninth Circuit

- nitrogen dioxide

- NMFS

- No Exposure Certification Identification Number

- No-Action Letter

- NOAA

- NOI

- NONA

- Nonapplicability Identification Number

- Nonattainment

- Nonpoint Source

- North American Electric Reliability Corporation

- North Dakota

- Notice

- Notice of Proposed Rulemaking

- NPDES

- NPDES Delegation

- NPDWR

- NPL

- NPRM

- NSPS

- NSR

- Nuclear

- Nuclear Energy

- NWP

- NY PSC

- Obama

- OBBB

- Occupational Safety and Health Act

- Occupational Safety and Health Administration

- OCE

- OECA

- OEHHA

- OEJECR

- Office of Civil Enforcement

- Office of Cybersecurity Energy Security and Emergency Response

- Office of Electricity Delivery & Energy Reliability

- Office of Enforcement and Compliance Assurance

- Office of Enforcement and Compliance Assurance (OECA)

- Office of Environmental Justice and External Civil Rights

- Office of Federal Register

- Office of Information and Regulatory Affairs

- Office of Management and Budget

- Office of Natural Resources

- Office of Water

- Offshore Energy

- Offshore Platforms

- Offshore Wind

- Offshore wind energy

- Ohio

- Oil

- Oil & Gas

- Oil and Gas

- Oil and Gas Production

- Oil and Gas Wastewater

- Oil Pipelines

- Oil Pollution Act

- OIRA

- Oklahoma

- OMB

- One Federal Decision

- One Federal Plan

- OPA

- Oregon

- OSHA

- Outer Continental Shelf

- OW

- Ozone

- Pacific OCS Region

- Packaging

- Paperwork Reduction Act

- Paris Agreement

- Paris Climate Accord

- Paris Climate Agreement

- Particulate Matter

- Partido Revolucionario Institucional

- Passaic River

- PATH Act

- PBT

- PCBs

- PEMEX

- Penalties

- Penalty

- PennEast Pipeline

- Pennsylvania

- Perfluoroalkyl

- Permian Basin

- Permitting

- Pesticide Devices

- Pesticides

- Pete Buttigieg

- Petition

- Petition for Rulemaking

- Petitions for Objection

- PetraNova

- Petrochemical Regulation

- Petróleos Mexicanos

- Petroleum Products

- PFAS

- PFAS Action Plan

- PFAS in Products State Law Tracker

- PFAS Reporting Rule

- PFAS Strategic Roadmap

- PFBA

- PFBS

- PFNA

- PFOA

- PFOS

- PHMSA

- Physicians for Social Responsibility

- Pimphales Promelas

- PIP

- Pipe Manufacturing

- Pipeline

- Pipeline and Hazardous Materials Safety Administration

- Pipeline Attacks

- Pipeline Construction

- Pipeline Safety

- Pipelines

- PIPES

- Plastic

- Plastic Carryout bag

- PNAS

- POCSR

- Point Source

- Point Source Discharge

- Policy

- Policy Statement

- Pollution

- Pollution Exclusion

- Pollution Liability

- Pollution Prevention for Healthy People and Puget Sound Act

- Polyalkyl

- Polyfluoroalkyl

- Port of Los Angeles

- Porter-Cologne Water Quality Control Act

- Potentially Responsible Party

- POTW

- PRA

- Practical Law

- Precedent

- Preconstruction Authorizations

- Preemption

- Prejudice

- Preliminary Injunction

- President Biden

- President Trump

- Presidential Transition

- PRGs

- PRI

- Priebus

- Principal

- Principles for Responsible Investments

- Priority Pollutants

- Privacy

- Process Safety Management

- Produced Water

- Product Packaging

- Product Safety

- Production Cuts

- Production Sharing Contract

- Prohibition on Sale

- Project Development

- Prop. 65

- Proposition 65

- Protected Species

- Protecting Our Conserved Lands Act of 2019

- PRP

- Pruitt

- Pruitt Task Force

- PSC

- PSD

- PSH

- PSM

- Public Comment

- Public Lands

- Public Utilities

- Publicly Owned Treatment Works

- Pumped Storage Hydropower

- PURPA

- Quality Assurance Plan

- R-Project Transmission Line

- Racing Vehicles

- RAGAGEP

- Railroad Commission

- Railroad Commission of Texas

- Railroad Commission of Texas (RRC)

- Rapanos

- RBI

- RCRA

- RCRA Subtitle D

- REACH

- Reasonable Progress Plans

- RECLAIM

- Reconsideration

- RECs

- Redevelopment

- Refinery

- Reform

- Reforma Energética

- Regional Clean Air Incentives Market

- Regional Clean Hydrogen Hubs

- Regional Greenhouse Gas Initiative (RGGI)

- Regional Haze

- Regional Water Quality Control Boards

- Registration Evaluation Authorization and Restriction of Chemicals

- Regulation

- Regulation and Enforcement

- Regulation S-K

- Regulation S-X

- Regulations

- Regulatory

- Regulatory Agenda

- Regulatory Freeze

- Regulatory Guidance

- Regulatory Programs

- Regulatory Reform

- Regulatory Review

- Reliability

- Reliability Safety Valve

- Remediation

- Removal Action

- Renewable

- Renewable Energy

- Renewable Energy Certificates

- Renewable Energy Portfolio

- Renewable Fuel Standards

- Renewable Portfolio Standard

- Renewables

- Renewals

- Reporting

- Request for Information

- ReRED

- Rescind

- Resilience of the Bulk Power System

- Resource Conservation and Recovery Act

- Responsible Business Initiative

- Restoration

- Restriction of Hazardous Substances

- Retail

- Retailers

- Retained

- Retroactivity

- Return on Equity

- RFS

- RHA

- Richard Glick

- Rigs to Reefs

- RIN

- Ripeness

- Risk and Technology Review

- Risk Assessment

- Risk Evaluation

- Risk Management

- Risk Management Plan

- Risk Management Program

- Risk Management Regulations

- Rivers and Harbors Act

- RMP

- Roadmap Release

- Roanoke River Basin Association

- Robert Powelson

- ROE

- ROEs

- RoHS

- Roundtable on Sustainable Palm Oil

- Roundup

- Royalties

- RPS

- RRBA

- RRC

- RTR

- Rule 14a-8(i)(7)

- Rule 65(c)

- Rulemaking

- Russia

- SAB

- Sackett

- Sacred Sites

- SAFE

- Safe Drinking Water Act

- Safe Harbor

- Safe Harbor Regulation

- Safe Harbor Warning

- Safer Consumer Products

- SAFETY Act

- Safety Management System

- San Francisco Bay Regional Water Quality Control Board

- SASB

- SaskPower’s Boundary Dam Unit 3

- SB 1371

- SCAQMD

- Science

- Science Advisory Board

- Science Advisory Board (SAB)

- Scope

- Scope 1

- Scope 2

- Scope 3

- Scott Pruitt

- SCOTUS

- SDWA

- SEC

- Section 10

- Section 104 Request

- Section 114 Request

- Section 179B(b)

- Section 208 Request

- Section 308 Request

- Section 4

- Section 401

- Section 404

- Section 408

- Section 45Q

- Section 5

- Section 6(b)

- Securities Act

- Securities and Exchange Commission

- Securities and Exchange Commission (SEC)

- Securities Law

- Seismicity

- Seminole Rock

- Senate

- Senate Energy and Natural Resources Committee

- Senator Lamar Alexander

- SEP

- SEPs

- Services

- Settlements

- Sewage

- Shareholder Lawsuits

- Shutdown

- Sierra Club

- Significant Figures

- Significant Guidance

- Significant New Use Rule

- SIP

- Smelter

- SNUR

- Social

- Social Media

- Solar

- Solid Waste

- South China Sea

- South Coast Air Quality Management District

- SPCC

- Species

- SPEED Act

- Spill Prevention Control and Countermeasure Rule

- SSB 5135

- SSM SIP Call

- Stabilization Clause

- Standing

- Standing Rock Sioux

- Stare Decisis

- State

- State Administrative Appeals

- State Air Pollution Control Board

- State Constitutions

- State Environmental Quality Review Act

- State Implementation Plan

- State Law

- State Water Resources Control Board

- States

- Statute

- Statute of Limitations

- Statutory Authority

- Statutory Interpretation

- Stormwater

- Strategic

- Straw Proposal

- Subrogation

- sulfur dioxide

- Sunset Review

- Superfund

- Supplemental Environmental Projects

- Supply Chain

- Supreme Court

- Supreme Court of Texas

- Supreme Court of the United States (SCOTUS)

- Surface Mining Act

- Surface Mining and Reclamation Act

- Surface Water Discharge

- Susan Bodine

- Sustainability

- Sustainability Accounting Standards Board

- Sustainable Development Goals

- Sustainable Investing

- SWDA

- Switzerland

- SWRCB

- Tailings Storage Facility

- Take

- Take Prohibition

- Takings

- Task Force on Climate-Related Financial Disclosures (TCFD)

- Tax

- Tax Credit

- Tax Credits

- Tax Cuts and Jobs Act

- Tax Reform

- Taxonomy Regulation

- TCEQ

- TCI

- Temporary Policy

- TERP

- Texas

- Texas Alliance of Energy Producers

- Texas Commission on Environmental Quality

- Texas Legislature

- Texas Railroad Commission

- Texas Water Development Board

- Thailand

- THC

- The European Commission

- The Mikado

- The Treasury Department

- The Water Infrastructure Improvements Act

- the WIIN Act

- Third Circuit

- Threatened Species

- Title V

- TMDL

- TMDLs

- TNALs

- Toledo

- Tolling Order

- Total Maximum Daily Load

- Toxic Chemicals

- Toxic Substances Control Act

- Toxic Substances Control Act (TSCA)

- Toxics

- Toxics Release Inventory

- Transcos

- Transition

- Transmission

- Transparency

- Transport

- Treasury

- Treaty Rights

- Trends

- TRI

- Tribal Rights

- Tribes

- Trump

- Trump Administration

- TSA

- TSCA

- TSF

- TWDB

- U.S. Army Corps of Engineers

- U.S. Environmental Protection Agency

- U.S. Senate

- Ultimate Net Loss

- UNCLOS

- Underground Injection Wells

- Underground Storage Tank

- UNFCCC

- Unified Agenda

- United Airlines

- United Nations

- United Nations Framework Convention on Climate Change

- Urgenda

- US Army Corps of Engineers

- US Chemical Safety Board

- US Climate Alliance

- US Court of Appeals for the Ninth Circuit

- US Customs and Border Protection

- US Department of Agriculture

- US Environmental Protection Agency

- US Environmental Protection Agency (EPA)

- US Fish and Wildlife Service

- US FWS

- US SAFETY Act

- US Securities and Exchange Commission

- US Securities and Exchange Commission (SEC)

- US Supreme Court

- USACE

- USDA

- USDOT

- USFWS

- USMCA

- Utilities

- Utility

- Vapor Intrusion

- Vapor Recovery Units

- VCP

- Venting

- Veto

- Village of Old Mill Creek. v. Star

- Vineyard Wind

- Virginia

- Virginia Clean Economy Act

- Virginia Community Flood Preparedness Fund

- Virginia Department of Environmental Quality

- Virginia State Corporation Commission

- Vision of Corporation Finance

- VOCs

- Volatile Organic Compounds

- Voluntary Cleanup Program

- Voluntary Remediation

- Waiver

- Waiver Period

- Warnings

- Washington

- Waste

- Waste Discharge Identification Number

- Waste Electrical and Electric Equipment

- Waste Permitting

- Wasted Food

- Wastewater

- Wastewater Treatment

- Water

- Water Quality Certification

- Water Quality Criteria

- Water Regulation

- Water Reuse

- Water Supply and Management

- Water Systems

- Waterfront

- Waters

- Waters of the United States

- WDID

- WEA

- WEEE

- Well Blowout

- Well Control Rule

- WET Tests

- Wetlands

- Whole Effluent Testing

- Wholesale Electricity

- WildEarth Guardians

- Wildfire

- Wind

- Wind Energy

- Wind Energy Area

- Wind Farms

- Winning on Reducing Food Waste Initiative

- Winter v. NRDC

- Withdrawal or Reinstatement

- World Bank Group Equator Principles

- Worst-Case Discharge

- WOTUS

- WQBELs

- WQC

- Wyoming

- Zero Emissions

- Zero-Emissions Vehicle Initiative

- Zinke

Authors

- Walter J. Andrews

- Fatima Anjum

- John J. Beardsworth, Jr.

- Jordan L. Bernstein

- Timothy E. Biller

- John R. Bobka

- George Borovas

- Lawrence J. Bracken II

- Shannon S. Broome

- Karma B. Brown

- Samuel L. Brown

- F. William Brownell

- Courtney Cochran Butler

- Aaron J. Carroll

- E. Carter Chandler Clements

- Benjamin Y. Cooper IV

- Eric S. Crusius

- Christopher J. Cunio

- Alexandra B. Cunningham

- Field Daniel

- Andrea DeField

- Douglas L. Dua

- Deidre G. Duncan

- Chloe Dupre

- Frederick R. Eames

- Kevin S. Elliker

- Clare Ellis

- Latosha M. Ellis

- Joanna D. Enns

- Geoffrey B. Fehling

- Hannah Flint

- Steven C. Friend

- Kevin E. Gaunt

- Andrew G. Geyer

- Roger C. Gibboni

- Sevren R. Gourley

- Elisabeth R. Gunther

- Steven M. Haas

- Alexandra Hamilton

- James W. Head

- Patrick Jamieson

- Kevin W. Jones

- Laura Ellen Jones

- Dan J. Jordanger

- Ryan T. Ketchum

- Jonathan H. Kim

- Scott H. Kimpel

- Abigail Klauer

- Charles H. Knauss

- J. Pierce Lamberson

- Lucinda Minton Langworthy

- Charlotte E. Leszinske

- Brian R. Levey

- Michael S. Levine

- Elbert Lin

- Eric R. Link

- David S. Lowman, Jr.

- Erika Maley

- Sadie Mapstone

- James Martin

- Jeffrey N. Martin

- Lorelie S. Masters

- Patrick M. McDermott

- Kerry L. McGrath

- Robert J. McNamara

- Nathan R. Menard

- Michael J. Messonnier, Jr.

- Todd S. Mikolop

- Angela Morrison

- Michael J. Mueller

- Eric J. Murdock

- Ted J. Murphy

- William L. Newton

- Paul T. Nyffeler, PhD

- Peter K. O’Brien

- G. Michael O’Leary

- Evangeline C. Paschal

- Kate Perkins

- Shemin V. Proctor

- Myles F. Reynolds

- Doris Rodríguez

- Brent A. Rosser

- Rachel Saltzman

- Arthur E. Schmalz

- Penny A. Shamblin

- Michael R. Shebelskie

- George P. Sibley, III

- Joseph C. Stanko

- Brian T. Stansbury

- Martin P. Stratte

- Javaneh S. Tarter

- Thomas W. Taylor

- David Arthur Terry

- Linda Trees

- Andrew J. Turner

- Emily Burkhardt Vicente

- Carl von Merz

- Ayesha K. Waheed

- Gregory R. Wall

- Daniel C. Warren

- Thomas R. Waskom

- Malcolm C. Weiss

- Susan F. Wiltsie