October began with a CPSC announcement that a major retailer agreed to pay a $3.85M civil penalty for failing to report that a trash can it sold contained a defect or created an unreasonable risk of serious injury. The retailer sold 367,000 of the trash cans nationwide between December 2013 and May 2015. Allegedly the trash can’s plastic collar may dislodge, exposing a sharp edge and posing a laceration hazard to consumers. The retailer received 92 consumer complaints about this alleged defect but did not immediately notify the CPSC of the defect. The CPSC announced a recall of the trash can in July 2015. In addition to the civil penalty, the retailer agreed to maintain a compliance program and a system of internal controls and procedures to ensure it discloses information to the CPSC in accordance with applicable law. The Commission voted unanimously (4-0) to accept the settlement.

With this civil penalty, the CPSC has assessed four civil penalties in 2018 for a record-breaking total of $37.6M. The prior record was established in 2016, when the CPSC collected $37.3M via six civil penalties. With two months left in the calendar year, the 2018 total for civil penalties may further increase. This civil penalty also marks the first multi-million dollar civil penalty since the recent change in political make-up of the Commission from a majority of Democratic appointees to a majority of Republican appointees. This suggests that regardless of the political make-up of the Commissioners, the agency will not abandon use of the civil penalty as part of its enforcement arsenal when presented with convincing evidence that a manufacturer, distributor or retailer failed to comply with legal reporting requirements.

October’s most noteworthy recall involved pressure-assisted flushing systems — a key component for flushing toilets. The system “can burst at or near the vessel weld seam releasing stored pressure.” This released pressure can lift the tank’s lid and/or shatter the tank, posing a serious laceration hazard. The manufacturer has received over 1,400 reports of the systems bursting, injuring 23 consumers and causing over $700,000 in property damage. In response, the manufacturer recalled 1.4 million units. This is recall adds to the manufacturer’s prior recalls of similar systems in June 2012, January 2014 and July 2016.

Attorneys from Hunton Andrews Kurth LLP’s Insurance Coverage practice group weigh in on two contamination and recall insurance disputes.

In Lake Country Foods' case (previously discussed in the May Recall Roundup), the insurer has filed counterclaims against Lake Country Foods (“LCF”) seeking reimbursement of the approximately $1.2 million advance payment it made in connection with an alleged salmonella contamination incident at one of LCF’s facilities. LCF had sought an order permitting it to keep $1.2 million already paid by the insurer and requiring the insurer to provide coverage for the product contamination claim. In response, the insurer has raised numerous defenses disputing any obligation to provide coverage and has also filed counterclaims against LCF seeking to void the policy and order LCF to return the $1.2 million advance payment. In support of these claims, the insurer asserts that LCF was aware of the salmonella contamination and adverse FDA inspection reports at the time it submitted an application stating it had no knowledge of circumstances that may lead to an insured loss, and that its facilities had not been the subject of regulatory recommendations or complaints. The insurer alleges that had LCF not concealed the truth, it would have not made the advance payment and would have been justified in denying the claim in full under the policy. We will continue to monitor the case for further developments.

In Amalgamated Sugar Co. v. The Cincinnati Insurance Co., Amalgamated Sugar Co. ("Amalgamated"), the second-largest sugarbeet processor in the United States, filed a coverage lawsuit against its commercial general liability insurer seeking to recover more than $1 million in losses sustained by customers that received contaminated sugar products. Amalgamated alleges that it entered into a written agreement with a company (D&S Ingredient Transfer Company, Inc., or “D&S”) to process and deliver Amalgamated’s sugar products to customers. In October 2014, Amalgamated discovered during quality control testing that the sugar products that D&S processed and delivered to Amalgamated’s customers had become contaminated with excess amounts of chlorine. While not dangerous or hazardous, the produced were irreparably damaged, could not be sold to consumers, and were destroyed. Three customers demanded that Amalgamated compensate them for more than $1 million in losses they incurred due to the damaged sugar shipments, including the cost of the sugar they purchased, processing their products with the damaged sugar, disposing of the damaged sugar products and remediating their contaminated facilities.

Amalgamated provided notice of a claim under its commercial general liability and umbrella policies issued by Cincinnati, asserting that Cincinnati was obligated to provide coverage for property damage under various coverage parts, including property damage resulting from “your work.” Cincinnati acknowledged the claim and funded and controlled an arbitration against D&S related to its role in processing and distributing the contaminated products. Amalgamated alleges that for the next several years, Cincinnati continued to acknowledge partial coverage for the claim by pursuing the arbitration against D&S, but in October 2018 “reversed course” and denied coverage only one month before the arbitration hearing. Due to Cincinnati’s withdraw of coverage, Amalgamated brought a lawsuit asserting claims for breach of contract, bad faith and declaratory judgment on the grounds that it was entitled to coverage for the claim, and that Cincinnati denied coverage “at the eleventh hour” and “disingenuously and in bad faith blamed Amalgamated for the fact that its customers unilaterally addressed their claims by taking offsets to amounts they owe Amalgamated after [Cincinnati] did nothing to resolve Amalgamated’s liability.” Amalgamated asserts that Cincinnati was entirely focused on shifting its own responsibilities for resolving liability onto D&S and its insurer, thereby placing its own interests ahead of its insured, Amalgamated.

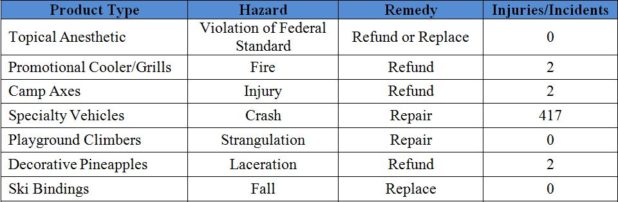

Total Recalls: 33

Hazards: Fire/Burn/Shock (11); Fall (6); Injury (3); Laceration (3); Crash (3); Violation of Federal Standard (2); Drowning (2); Choke (1); Strangulation (1); Risk of Head Injury (1)

Click on the below chart for additional information.

Partner

PartnerSyed represents clients in connection with insurance coverage, reinsurance matters and other business litigation. Syed serves as the head of the firm’s insurance coverage practice. He has been admitted to the US Court of Appeals ...

Partner

PartnerKelly practices as a commercial and regulatory litigator on products liability and post M&A disputes and issues and serves as one of the firm’s Deputy General Counsel focusing on law firm ethics, conflicts, and risk management ...

Partner

PartnerGeoff works closely with corporate policyholders and their directors and officers to resolve high-stakes insurance disputes. He leads the firm’s directors and officers (D&O) insurance and executive protection practice.

As a ...

Search

Recent Posts

Categories

- Advertising & Marketing

- Bankruptcy

- Class Action

- Competition/Antitrust

- Consumer Protection

- Corporate Governance

- Environmental

- General

- Health Care

- Insurance

- IP

- Labor and Employment

- Mergers & Acquisitions

- News & Events

- Patent Infringement

- Patents

- Privacy & Cybersecurity

- Product Liability

- Real Estate

- Regulatory

- Technology & E-Commerce

Tags

- 29 C.F.R. § 785.48

- 396-r

- 3D Printer

- 3D Printing

- A. Todd Brown

- A.S. Research (ASR)

- Aaron P. Simpson

- Accountability

- Administrative Agencies

- Administrative Exemption

- Advertisers

- Advertising

- Advertising Claims

- Advertising Guidelines

- Advertising Idea

- Agency Guidance

- Agency Principles

- AI Interviewing Platforms

- AI Technology Reviews

- AIA

- Air

- Algorithmic Accountability Act

- Align

- Americans with Disabilities Act

- Americans with Disabilities Act (ADA)

- Andrea DeField

- Ann Marie Buerkle

- Annual Reports

- anti-aging

- Anti-Competitive Marketplace

- Anti-Discrimination

- APEX Agreement

- Arbitration

- Arbitration Agreements

- Arizona

- Arkansas

- Arthritis

- Artificial Intelligence (AI)

- Asbestos

- Assembly Bill 51 (AB 51)

- ATDS

- Athlete Eligibility

- Australia

- Auto-renewals

- Automatic Telephone Dialing System (ATDS)

- Automobile

- Automotive Body Parts Association (ABPA)

- Back to Work Emergency Ordinance

- biased endorsements

- Biden Administration

- Biometric Data

- Biometric Information

- Biometric Information Privacy Act (BIPA)

- BIPA

- Bitcoin

- Blockchain

- Board Diversity Disclosure

- Boards of Directors

- Bonuses

- Braille

- Branding

- Breach

- Breach of Contract

- Business Interruption

- Business Interruption Loss

- Businessowner’s Insurance

- Buy Now, Pay Later

- California

- California Air Resources Board

- California Assembly Bill 2011

- California Employment Laws

- California Fair Employment and Housing Act

- California False Claims Act

- California Labor Code

- California Legislation

- California Senate Bill 6

- California’s Unfair Competition Law

- CalRecycle

- CAMS

- Canada

- Cannabis

- CARB

- CBD

- CBP

- CCPA

- Celebrity Endorsers

- Center for Disease Control (CDC)

- CFIUS

- CGL

- Chatbot

- Children’s Advertising

- Children’s Advertising Review Unit

- Children’s Online Privacy Protection Act (COPPA)

- China

- Christopher J. Dufek

- Christopher W. Hasbrouck

- Christy Kiely

- CIPA

- Class Action

- Class Action Litigation

- Class Actions

- Clawback

- Click-to-Cancel

- Climate Change

- Climate Disclosure

- clinical trials

- Collective Action

- Colorado

- Commerce Clause

- Commercial General Liability

- Commercial Leasing

- Commercial Messaging

- Commercial Products

- Commercial Real Estate

- Commodity Futures Trading Commission

- Compensation

- Compliance

- Confidentiality

- Congress

- Connecticut

- Consent

- Consent Order

- Consumer Advertising

- Consumer Data

- Consumer Financial Protection Bureau

- Consumer Fraud

- consumer loyalty program

- Consumer Privacy

- Consumer Product Safety Act

- Consumer Products

- Consumer Products Safety Commission (CPSC)

- Consumer Protection

- Consumer Review Fairness Act of 2016 (CRFA)

- Consumer Reviews

- Consumer Rights

- Contamination

- Contract Law

- Controlled Substance Act

- Cookies

- Cookware

- COPPA

- Copyright

- Coronavirus/COVID-19

- Corp Fin

- Corporate Governance

- Corporate Reporting

- Corporate Sustainability

- Corporate Transparency Act (CTA)

- Costco

- Counterfeit Goods

- Counterfeit Goods Seizure Act of 2019

- Court of International Trade

- CPPA

- CPRA

- CPSA

- CPSC

- Crack House Statute

- CRFA

- Crypto

- Cryptocurrency

- CSPA

- Cuba

- Currency

- Customs and Border Protection

- Cyber

- Cyber Coverage

- D. Andrew Quigley

- D&O

- D&O policies

- Damages

- Data Breach

- Davidson

- Deceptive Advertising

- DEI

- Delaware

- Delivery Drivers

- DEP

- Department of Agriculture

- Department of Justice

- Department of Labor

- Development Impact Fee

- Dietary Guidelines

- Digital Assets

- digital currency

- Disclosures

- Discrimination

- Distribution

- District of Columbia

- Division of Corporation Finance

- Dodd-Frank

- DOJ

- DOL

- Duty to Defend

- Duty to Indemnify

- e-liquid products

- Eddie Bauer

- EEOC

- Electric Vehicles

- Eleventh Circuit

- Emily Burkhardt Vicente

- Employee Rights

- Employment-Based Immigration

- Endorsement

- Endorsement Guides

- Endorsement Notice

- Endorsements

- endorser monitoring requirements

- Enforcement

- Environmental Impact

- Environmental Protection Agency

- Environmental Protection Agency (EPA)

- EPA

- Epidemic

- ESG

- ESG Disclosure

- EU Regulation

- European Union

- European Unitary Patent

- EV Charging

- Exceptions

- Exclusions

- Executive Compensation Disclosure Rules

- Executive Order (EO)

- Executive Orders

- Exercise Machines

- Extended Producer Responsibility (EPR)

- FAA

- Fair Labor Standards Act

- Fair Labor Standards Act (FLSA)

- fair use

- False Advertising

- False Advertising Claims

- False Advertising Law

- False Claims Act

- Family Leave Policies

- FAR

- Fashion Accountability Acts

- FCC

- FCRA

- FDA

- Federal Acquisition Regulations

- Federal Arbitration Act (FAA)

- Federal Communications Commission

- Federal Contractors

- Federal Contracts

- Federal District Court

- Federal Government Contractor

- Federal Government Shutdown

- Federal Trade Commission

- Federal Trade Commission (FTC)

- FFDCA

- FIFRA

- Fifth Circuit

- Final Rule

- Financial Technology

- FinCEN

- FinHub

- Fireworks

- First Amendment

- Fixing America’s Surface Transportation (FAST) Act

- Florida

- Florida House of Representatives (HB 963) and Florida Senate (SB 1670)

- Florida Legislature

- FLSA

- FLSA/Wage & Hour

- FMLA

- Food and Beverage Manufacturers

- Food and Drug Administration (FDA)

- Food Delivery

- Food Safety

- Form 10-K

- Formaldehyde Standards for Composite Wood Products Act of 2010

- fractional interests

- Franchise

- Frederic Chang

- Free Trials

- FTC

- FTC Act

- Gavin Newsom

- GDPR

- General Liability

- Geoffrey B. Fehling

- Georgia

- Gift Cards

- GoodRx

- Gramm-Leach-Bliley (GLB) Act

- Green

- Green Guides

- Greenhouse Gas

- Gun Safety

- Hart-Scott-Rodino

- Hart-Scott-Rodino (HSR)

- Hashtag

- Hawaii

- Health Care

- Health Claims

- Hedge Fund

- Higher Education

- HIPAA

- hoverboards

- human capital

- Human Rights

- IEEPA

- Illinois

- Illinois Artificial Intelligence Video Interview Act (the Illinois Act)

- Illinois Biometric Information Privacy Act (BIPA)

- Independent Contractors

- Indiana

- Indoor Mall

- Influencer Marketing

- Infringement

- initial public offerings (IPOs)

- Injury

- Insurance

- Insurance Loss

- Insurance Provider

- Intellectual Property

- Intellectual Property Licenses in Bankruptcy Act

- Inter Partes Review

- Interest Rate

- International

- International Trade Commission

- International Trade Commission (ITC)

- Internet

- Inventorship

- investigation

- INVISALIGN

- Iowa

- IP

- IPR

- Ireland

- IT

- ITC

- iTERO

- Job Posting

- Joint Employer

- Junk Fees

- Katherine Miller

- Kurt A. Powell

- Kurt G. Larkin

- Labeling

- Labeling Requirements

- Labeling Rules

- Labor

- Labor Code Private Attorneys General Act of 2004 (PAGA)

- Labor Organizing

- Labor Unions

- Land Use

- Landlord

- Latin America

- Lautenberg Act

- Lawsuit Reform Alliance of New York (LRANY)

- Lead

- Lease

- Legislation

- Leveraged Loans

- Liability Insurance Policy

- Liberty Insurance Corporation

- Liberty Mutual Fire Insurance Company

- LIBOR Discontinuation

- liquidity

- Litigation

- Live Chat

- Lost Profits

- Lost Sales

- Louisiana

- Luxury Gyms

- M&A

- Made in the USA

- Made in USA

- MagicSleeve

- Magnuson-Moss Warranty Act

- Magnuson-Moss Warranty Act (MMWA)

- Maine

- Malcolm C. Weiss

- Manufacturing

- Marketing

- Marketing Claims

- Maryland

- Massachusetts

- Matthew T. McLellan

- Maya M. Eckstein

- MD&A

- Medtail

- Membership cancellation

- Mergers & Acquisitions

- Metaverse

- MeToo Movement

- Mexico

- Michael J. Mueller

- Michael S. Levine

- microplastics

- Microplastics Litigation

- Minimum Wage

- Minnesota

- Minnesota Pollution Control Agency (MPCA)

- Misclassification

- Mislabeling

- Mission Product Holdings

- Missouri

- Mobile

- Mobile App

- Motoclick

- Multi-Family Housing Development

- Multi-Level Marketing Program (MLM)

- NAA

- NAD

- NASA

- Nasdaq

- National Advertising Division

- National Advertising Division (NAD)

- National Advertising Review Board

- National Collegiate Athletic Association (NCAA)

- National Labor Relations Act

- National Labor Relations Board

- National Products Inc.

- National Retail Federation

- Natural Disaster

- Nebraska

- Negligence Claims

- Neil K. Gilman

- Network Outage

- Nevada

- New Jersey

- New York

- New York City Department of Consumer and Worker Protection

- New York Department of Financial Services

- NHTSA

- NIL rights

- Ninth Circuit

- NLRA

- NLRB

- no-action request

- Non-Compete

- Non-Exempt

- Non-Exempt Employees

- non-fungible token (NFT)

- North Carolina

- Nutrition Labels

- Obama Administration

- Occupational Safety and Health Administration (OSHA)

- Occurrence

- Office of Labor Standards Enforcement

- Ohio

- Oklahoma

- Online Cash Providers

- Online Retailer

- Online Reviews

- Opinion Letters

- Opioids

- Opt-Out

- Oregon

- Overboarding

- Overtime

- Overtime Exemptions

- Ownership

- Packaging

- PAGA

- Pandemic

- Patent

- Patent Infringement

- Patents

- Paul T. Moura

- Pay Equity

- Pay Ratio

- Pay Transparency

- Pay-To-Play Rankings

- Penalty

- Pennsylvania

- Penny Shortage

- Personal and Advertising Injury

- Personal Data

- Personal Information

- Personal Injury

- Personally Identifiable Information

- Pesticides

- PFAS

- Physical Loss or Damage

- Policy

- Predictive Inventory

- price gouging

- Primary and Umbrella Policies

- Privacy

- Privacy Guidelines

- Privacy Policy

- Privacy Protections

- Procurement

- Product Liability

- Product Packaging

- Product Safety

- Prohibition on Sale

- Property Insurance

- Property Rights

- Proposed Legislation

- Proposed Rule

- Proposition 65

- Proxy Access

- proxy materials

- Proxy Statements

- PTAB

- PTO

- Public Accommodations

- Public Companies

- Purdue Pharma

- Randall S. Parks

- Ransomware

- Real Estate

- Recall

- Recalls

- Recording

- Regulation

- Regulation S-K

- Restaurants

- Restrictions

- Restrictive Covenants

- Retail

- Retail Developers

- Retail Development

- Retail Industry Leaders Association

- Retail Litigation Center

- Retail Year in Review

- Retaliation

- Rounding

- Rulemaking

- Ryan A. Glasgow

- Sales Tax

- Salesforce

- SD8 coins

- SEC

- SEC Disclosure

- Second Circuit

- Section 337

- Section 365

- Secure and Fair Enforcement Banking Act of 2019 (“SAFE Banking Act”)

- Securities

- Securities and Exchange Commission

- Securities and Exchange Commission (SEC)

- Securities Exchange Commission

- security checks

- Self-Checkout

- Senate

- Senate Data Handling Report

- Sergio F. Oehninger

- Service Contract Act (SCA)

- Service Interruption

- Service Provider

- SHARE

- Shareholder

- Shareholder Proposals

- Sign-In Wrap Agreement

- Slogan

- Smart Contracts

- SNAP

- Social Media

- Social Media Influencers

- Software

- South Carolina

- South Dakota

- Special Purpose Acquisition Companies (SPACs)

- Sponsors and Gifting

- Sponsorship

- State Attorneys General

- State Law

- State Legislation

- Store Closures

- Strategic Plan

- Subscription Services

- Substantiation

- Substantiation Notice

- Supplier

- Supply Chain

- Supply contracts

- Supply-Chain Operations

- Supreme Court

- Surveillance Pricing

- Sustainability

- Syed S. Ahmad

- Synovia

- Targeted Advertising

- Tariff

- Tax

- TCCWNA

- TCPA

- Technology

- Technology Innovation

- Telemarketing

- Telephone Consumer Protection Act

- Telephone Consumer Protection Act (TCPA)

- Tempnology LLC

- Tenant

- Tennessee

- Terms and Conditions

- Texas

- The Fair Credit Reporting Act (FCRA)

- Third Party Litigation Funding

- Third-Party

- Thomas R. Waskom

- Title VII

- Tokenization

- Tokens

- Toxic Chemicals

- Toxic Substances Control Act

- Toxic Substances Control Act (TSCA)

- Trade Dress

- Trademark

- Trademark Infringement

- Trademark Trial and Appeal Board (TTAB)

- TransUnion

- Travel

- Trends

- Trump Administration

- TSCA

- TSCA Title VI

- U.S. Department of Justice

- U.S. Department of Labor

- U.S. Food and Drug Administration

- U.S. House of Representatives

- U.S. Patent and Trademark Office

- Ultra-Processed Foods

- Umbrella Liability

- Unfair and Deceptive Use

- Union

- Union Organizing

- United Specialty Insurance Company

- Unmanned Aircraft

- Unruh Civil Rights Act

- UPSTO

- US Chamber of Commerce

- US Customs and Border Protection (CBP)

- US Department of Agriculture

- US Environmental Protection Agency (EPA)

- US International Trade Commission (ITC)

- US Origin Claims

- US Patent and Trademark Office

- US Patent and Trademark Office (USPTO)

- US Supreme Court

- USDA

- USPTO

- Utah

- Varidesk

- Vendor

- Vermont

- Virginia

- Volatile Organic Compound (VOC) Emissions

- W. Jeffery Edwards

- Wage and Hour

- Wage-And-Hour

- Walter J. Andrews

- Warning Labels

- Warranties

- Warranty

- Washington

- Washington DC

- WCAG

- Web Accessibility

- Website

- Website Accessibility

- Weight Loss

- Wiretap

- Wiretapping

- World Health Organization (WHO)

- Wyoming

- Year In Review

- Zoning

- Zoning Conversion

- Zoning Ordinances

- Zoning Regulations

Authors

- Gary A. Abelev

- Christian S. Adams

- Syed S. Ahmad

- Brandon Bell

- Fawaz A. Bham

- Michael J. “Jack” Bisceglia

- Jennifer L. Bloom

- Jeremy S. Boczko

- Brian J. Bosworth

- Shannon S. Broome

- Samuel L. Brown

- Tyler P. Brown

- Melinda Brunger

- Jimmy Bui

- M. Brett Burns

- Daniel J. Butler

- Matthew J. Calvert

- Grant H. Cokeley

- Eric S. Crusius

- Christopher J. Cunio

- Alexandra B. Cunningham

- Merideth Snow Daly

- Timothy G. Decker

- Katherine P. Deegan

- Andrea DeField

- John J. Delionado

- Stephen P. Demm

- Mayme Donohue

- Christopher J. Dufek

- Robert T. Dumbacher

- M. Kaylan Dunn

- Chloe Dupre

- Frederick R. Eames

- Andre Earls

- Maya M. Eckstein

- Rob Edwards

- Tara L. Elgie

- Clare Ellis

- Latosha M. Ellis

- Juan C. Enjamio

- Kelly L. Faglioni

- Ozzie A. Farres

- Geoffrey B. Fehling

- Jason Feingertz

- Hannah Flint

- Erin F. Fonté

- Kevin E. Gaunt

- Jane M. Geiger

- Andrew G. Geyer

- Armin Ghiam

- Neil K. Gilman

- Ryan A. Glasgow

- Tonya M. Gray

- Elisabeth R. Gunther

- Steven M. Haas

- Kevin Hahm

- Jason W. Harbour

- Jeffrey L. Harvey

- Christopher W. Hasbrouck

- Eileen Henderson

- Gregory G. Hesse

- Kirk A. Hornbeck

- Jamie Zysk Isani

- Nicole R. Johnson

- Roland M. Juarez

- James A. Kennedy, II

- Suzan Kern

- Jason J. Kim

- Scott H. Kimpel

- Elizabeth King

- Abigail Klauer

- Leslie W. Kostyshak

- P. Reiko Koyama

- Kurt G. Larkin

- Tyler S. Laughinghouse

- Gerry Leone

- Michael S. Levine

- Ashley Lewis

- Abigail M. Lyle

- Maeve Malik

- Sadie Mapstone

- Eric R. Markus

- John Gary Maynard, III

- Gray Moeller

- Reilly C. Moore

- Michael D. Morfey

- Ann Marie Mortimer

- Michael J. Mueller

- J. Drei Munar

- Matthew Nigriny

- Michael A. Oakes

- Justin F. Paget

- Randall S. Parks

- J. Steven Patterson

- Katherine C. Pickens

- Gregory L. Porter

- Robert T. Quackenboss

- D. Andrew Quigley

- Michael Reed

- Natalie Reed

- Jonathan D. Reichman

- Kelli Regan Rice

- Patrick L. Robson

- Amber M. Rogers

- Zachary Roop

- Adam J. Rosser

- Rachel Saltzman

- Natalia San Juan

- Arthur E. Schmalz

- Raymond Schorr

- Daniel G. Shanley

- Madison W. Sherrill

- Nikki Skolnekovich

- Kevin V. Small

- J.R. Smith

- Bennett Sooy

- Brian T. Stansbury

- Daniel Stefany

- Hak Stepanyan

- Javaneh S. Tarter

- Shauna R. Twohig

- Paige Van Oosten

- Jessica N. Vara

- Emily Burkhardt Vicente

- Mark R. Vowell

- Gregory R. Wall

- Thomas R. Waskom

- Malcolm C. Weiss

- Holly H. Williamson

- Samuel Wolff

- Jingyi “Alice” Yao

- Jessica G. Yeshman